The Occupier Blueprint Volume 3: Workplace ROI: When the Workstation, Workplace, and Building Align

Workplace ROI: When the workstation, workplace, and building align

For the past several years, the conversation around offices for occupiers has largely centered on contraction. Employers are reducing footprints, increasing flexibility, and lowering occupancy costs. Across the country, companies gave back space, vacancy rose, and new development slowed sharply. That was a rational response to a market shaped by uncertainty and changing workplace patterns.

In 2026, with new supply constrained and many businesses returning to growth, occupiers are approaching the office differently than they did five years ago. The workplace is no longer viewed simply as overhead. It is increasingly being evaluated as a strategic tool that can help attract and retain talent, strengthen culture, and impress clients.

If leadership wants people back in the office more often, is the workplace experience actually supporting that goal? As AI and hybrid work continue to reshape how work gets done, office strategy has to do more than house employees. It must reduce friction, support collaboration, and create an environment people see value in returning to.

Is your strategy aligned?

The answer starts with understanding why employees come in, and what the data says about the gap between intention and experience.

Why do employees come to the office?

A recent Franklin Street team workplace strategy study found that employees primarily value the office as a place to collaborate, host clients, and build professional and social relationships. The top responses were collaboration at 70%, meeting with clients at 56%, and fostering professional and social connections at 53%. In other words, employees are not coming in just to sit at a desk. They are coming in for interactions that are harder to replicate remotely.

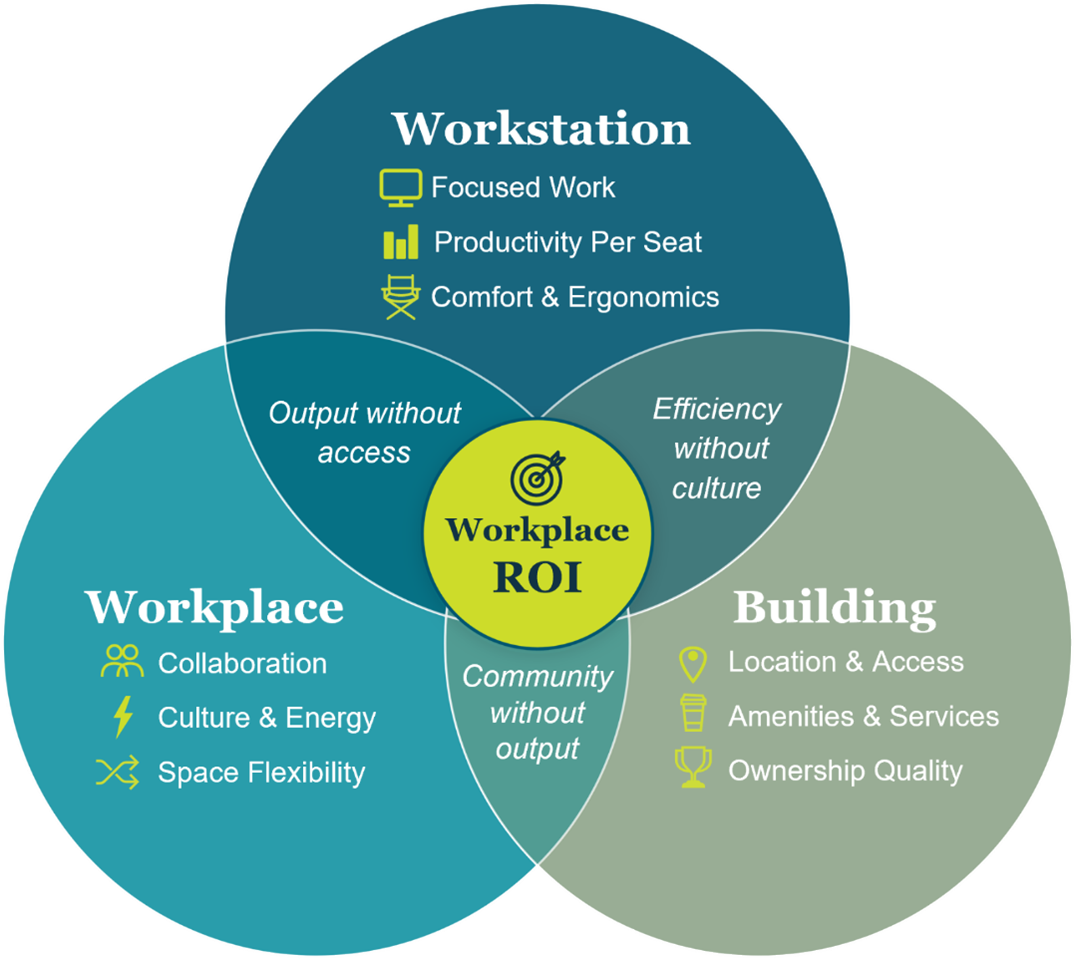

How should the workplace support collaboration?

The same study found that employees value flexibility and a range of space types that support how they work throughout the day. When asked where they prefer to collaborate, responses were split across the office, with 22% preferring their desk, 33% preferring large meeting rooms, and 35% preferring huddle rooms. That distribution suggests there is no single ideal setting. Effective workplaces offer variety.

That preference for collaboration and variety also showed up in how employees described the environments where they want to spend time. In open-ended comments about office usage and sustainability, respondents highlighted healthy food options, informal spaces to connect beyond the desk, and better spaces for company gatherings and events. The message is clear: companies asking more of the office also need the office to deliver more in return.

Beyond the workplace

While many of these preferences show up at the individual workstation and workplace levels, they are also shaped by the building itself. The broader office experience is influenced not just by what happens inside the suite, but by the amenities, services, and shared environments that surround it. As employees place more value on convenience, wellness, and flexibility, the standard for what makes a building feel supportive and worth commuting to is rising.

As a result, many building amenities that were once considered extras are increasingly becoming part of the baseline expectation. Convenient food service and gathering spaces such as coffee shops, restaurants, conference centers, and hospitality-driven common areas now play a meaningful role in fostering professional and social connection during the workday. Features such as fitness centers and small-format retail can further shape whether the office feels aligned with employee routines. The building is not separate from the workplace experience but rather, a part of it.

Avoiding the location trap

A building decision is not just a location decision. It’s a long-term commitment to an owner, an operating approach, and a level of capital support. Not all landlords are equally positioned, or equally motivated, to invest in the experience tenants now need. If ownership is not aligned with that standard, the workplace can fall short even if the suite itself is well designed.

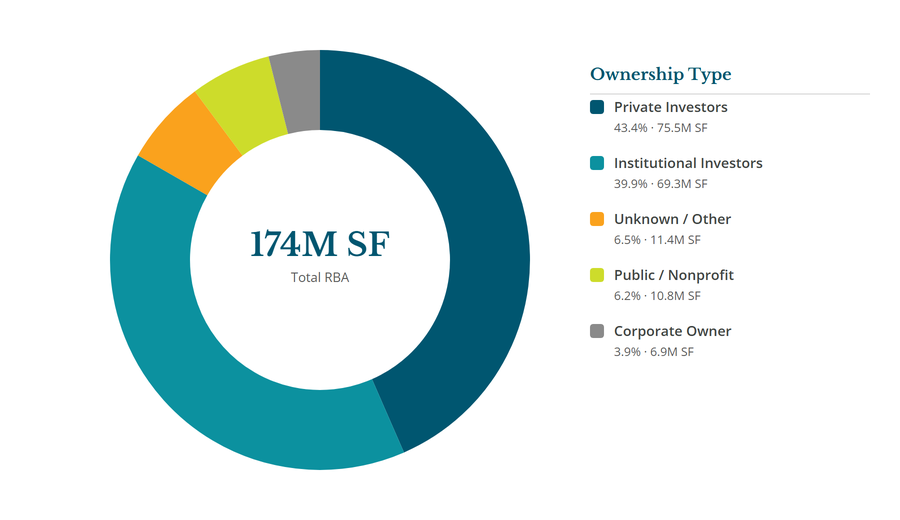

Looking at Atlanta’s office market, which is representative of many office markets, a large share of building ownership is controlled by institutional landlords, REITs, investment managers, and corporate owners. That matters because different ownership groups bring different capital structures, return thresholds, and investment horizons. In a market where the workplace experience is becoming more important to location decisions, those differences can materially affect a building’s ability to stay competitive.

As a result, the gap between buildings is becoming more visible. With much of the market being reset, properties backed by well-capitalized ownership are often better positioned to upgrade amenities, refresh common areas, and deliver the kind of environment tenants increasingly need to support attendance, culture, and collaboration.

For occupiers, the real question is whether their current space and building are keeping pace with employee expectations or quietly falling behind them. That is where Franklin Street can help. We work with companies to benchmark their workplace against the market, identify where the space or building may be creating friction, and find solutions to turn the office into a stronger tool for attracting talent, supporting culture, and improving workplace ROI.

What sets your office apart?

What makes your office a place people want to come to, and what is one thing that may be making it easier to stay away? If you would like to benchmark your current space against the market, we are glad to start that conversation.